In a previous post, we discussed Arkansas marketplace enrollment data showing that during the 2026 open enrollment period, premiums increased and consumer plan selection shifted, with many consumers rejecting silver-tier plans in favor of gold-tier plans. In this post, we take a closer look at the shifts in consumer plan selection, including data showing there was a substantial increase in consumers shopping around for better deals.

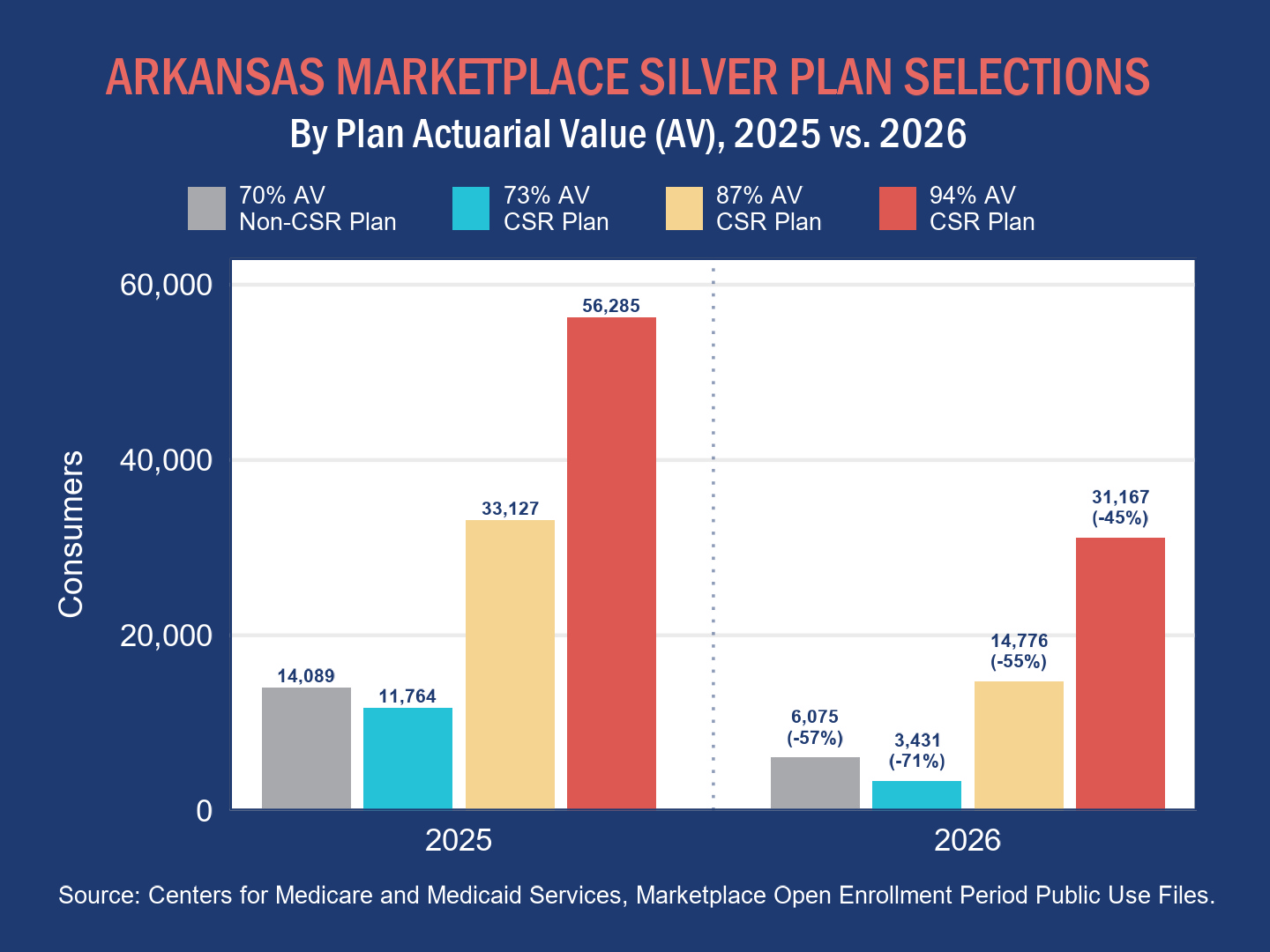

Movement Away From Plans With Cost-Sharing Reductions

Whether moving from a silver plan to a gold plan was more financially attractive for an enrollee depended largely on the enrollee’s income. Consumers with incomes (calculated as percentages of the federal poverty level, or FPL) that fall within certain brackets qualify for silver plans with varying levels of cost-sharing reductions (CSRs, called “extra savings” in healthcare.gov marketing), which reduce out-of-pocket costs for care. CSRs do not reduce plan premiums, however, so consumers facing premium increases for silver plans had reason to consider other plan options.

SILVER PLAN VARIETIES

| Actuarial Value | Eligible Income Bracket (FPL) | Eligible Income Bracket (2026) |

|---|---|---|

| 70% | >250% | >$39,126 |

| 73% | 200%-250% | $31,301-$39,125 |

| 87% | 150%-200% | $23,476-$31,300 |

| 94% | 100%-150% | $15,650-$23,475 |

In effect, silver plans can be thought of as coming in four varieties, defined by actuarial value (AV) — the percentage of healthcare expenses the plan covers for its average enrollee. A higher actuarial value means lower deductibles, copays, coinsurance, and/or out-of-pocket maximums. An enrollee will only qualify for one of the varieties, and premiums are the same across all varieties.

For consumers with 70% AV non-CSR silver plans and those with 73% AV silver plans with CSRs, a move to a gold plan for 2026 meant more generous coverage (about 80% AV), likely for no or little additional cost over their 2025 premium. For consumers with CSR silver plans with actuarial values of 87% or 94%, the move generally meant higher out-of-pocket costs at the point of care. While enrollment declined across all silver plan variations, the largest drops in terms of numbers of consumers were in CSR plans with actuarial values of 87% or 94%, indicating that many Arkansans with low incomes were pushed into plans with less financial protection in 2026.

More Consumers Actively Shopped for Plans

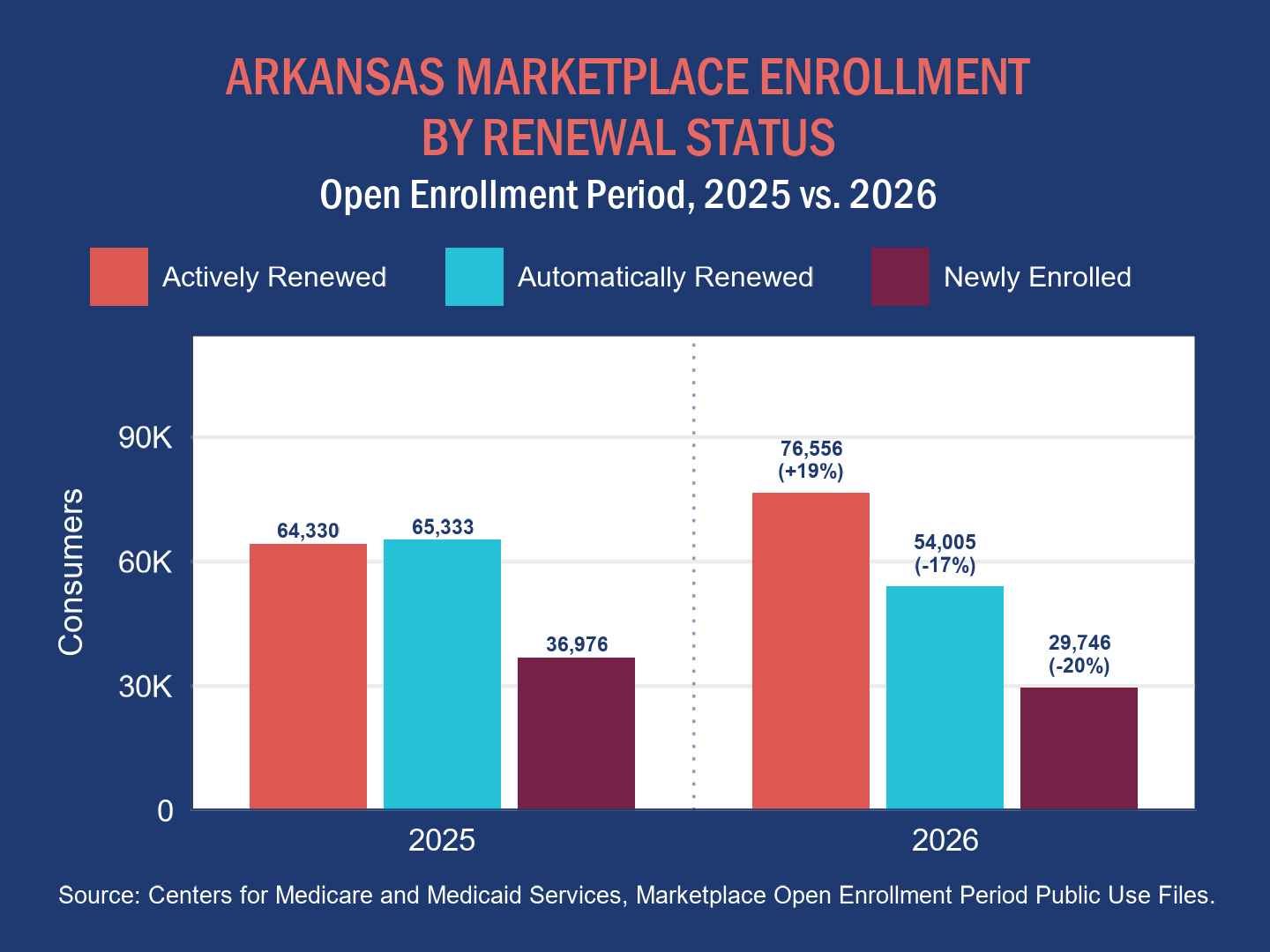

With sizable changes in plan premiums and the expiration of the enhanced tax credits, consumers had ample reason to shop around for new plans for 2026.

As shown in the graph below, the number of consumers who actively renewed coverage (i.e., they manually selected a plan on Healthcare.gov) rose substantially, whereas the number of consumers whose plans automatically renewed declined. There was also a relatively low number of new marketplace enrollees in 2026.

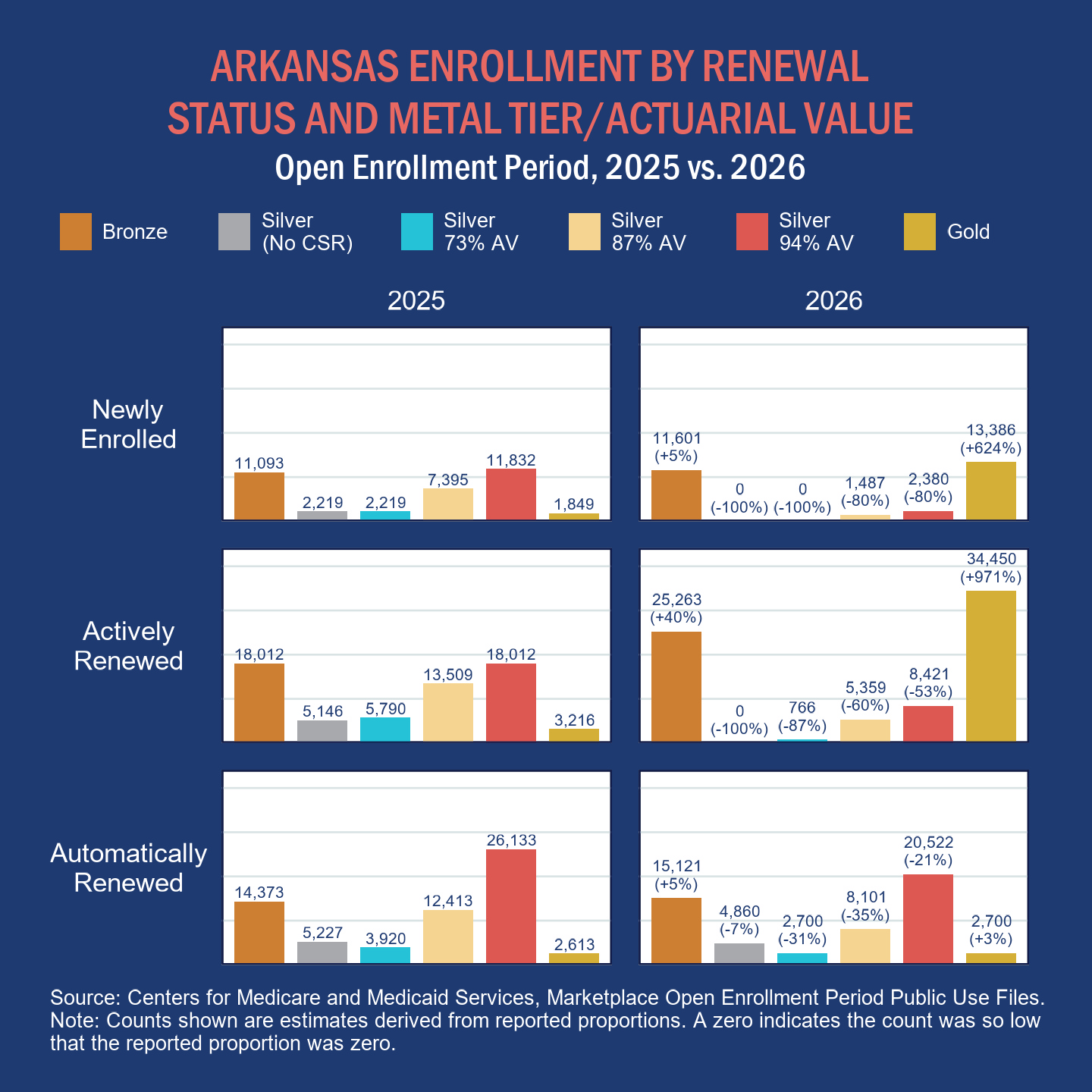

Looking across renewal groups, enrollment in non-CSR silver plans and CSR silver plans with 73% actuarial value occurred mostly among consumers whose coverage was automatically renewed, as shown in the graph below. Consumers who actively shopped for plans, including new enrollees, selected standard silver plans far less frequently than they did in 2025, tending most often to select gold plans instead.

When shopping for marketplace coverage, consumers must balance monthly premiums against generosity of cost-sharing protections to decide on a plan. This means considering advance premium tax credits — federal subsidies that reduce monthly premiums for enrollees with low incomes — and the availability of CSRs. The options available to consumers vary widely depending on their income.

The interactive tool below helps to illustrate the plan pricing that drove changes in consumer plan selection in 2026. The tool displays the premium of the lowest-cost plan in each metal tier, before and after application of the advanced premium tax credit, for hypothetical consumers at several different income levels.