Each year, the Centers for Medicare and Medicaid Services publishes a set of public use data files containing state- and county-level information about consumers’ premiums and plan selections on the Affordable Care Act marketplaces during the annual open enrollment period. We previously used these data to create a dashboard on Arkansas marketplace plan selections and premiums for the open enrollment periods of 2020 through 2026 and noted key takeaways in the 2026 data, including a modest decline in enrollment, a shift in the types of plans selected, and an increase in average premiums. This post, the first in a series, examines the data in greater detail to better understand those shifts.

Modest Decline in Overall Enrollment

Nationwide, marketplace plan enrollment fell 4.9% in 2026 compared to the previous year, but decreases varied across states. In Arkansas, enrollment declined by 3.8%, with most of this decline occurring among those with incomes below 200% or above 400% of the federal poverty level.

These numbers represent plan selections as of the end of the 2026 open enrollment period (January 15, 2026, in Arkansas), not effectuated coverage, meaning that consumers had not necessarily paid their first premiums when the data were collected. According to more current enrollment data from the Arkansas Insurance Department, 10.1% of enrollees dropped coverage between February and April 2026, more than double the 4.9% who dropped coverage in that time frame in 2025. Marketplace enrollment as of April 2026 stood at 134,310, which was down by 12% from the same time last year.

Shift Away From Silver Plans Driven by Premium Changes

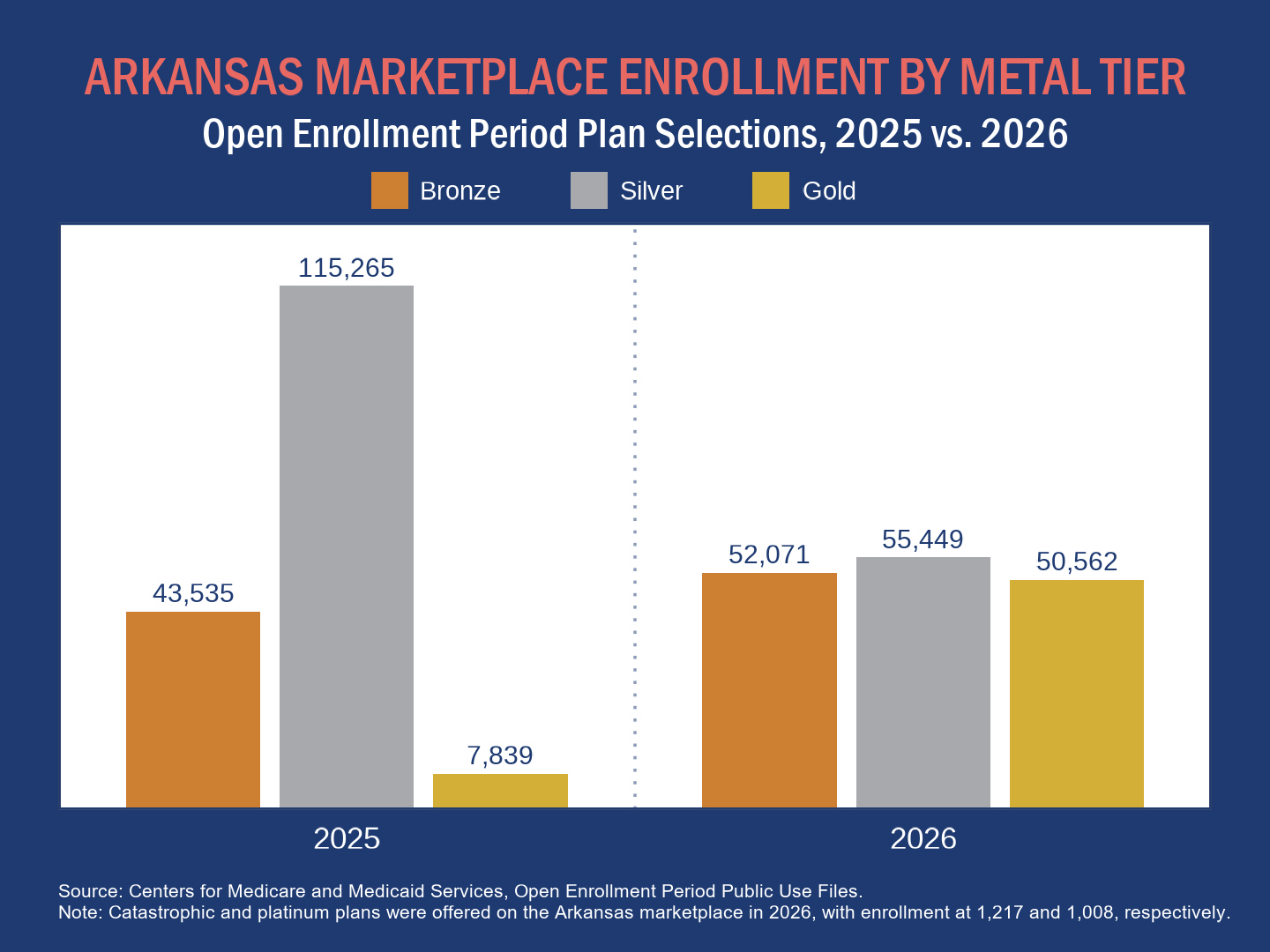

While overall enrollment in Arkansas as of the end of the open enrollment period for 2026 was down only 3.8% from the previous year, consumer plan preference showed a major shift compared to 2025.

Marketplace plans are divided into five categories — catastrophic, bronze, silver, gold, and platinum — based on the portion of healthcare expenses they cover. The latter four are commonly called “metal tiers,” and the vast majority of consumers select plans from the bronze, silver, or gold tiers. Of these three, bronze plans have the lowest premiums but the highest deductibles and cost-sharing requirements, gold plans have the highest premiums but the lowest deductibles and cost-sharing requirements, and silver plans lie in-between.

Platinum plans generally have even lower deductibles and cost-sharing requirements than gold plans, but they have very high premiums. Platinum plans were available on the Arkansas marketplace for the first time in 2026, but few consumers selected these plans. Catastrophic plans are an alternative option for certain qualifying consumers; the plans have low premiums but very high deductibles and cost-sharing requirements, and they are not eligible for federal premium subsidies. Despite recent federal action expanding access to catastrophic plans, few Arkansans selected the one catastrophic plan available on the marketplace in 2026.

Notably, enrollment in silver plans halved in Arkansas in 2026, while enrollment in gold plans soared and enrollment in bronze plans increased somewhat. The shift away from silver plans presumably reflects strategic changes in plan pricing that insurers made in response to rising healthcare costs and the expiration of enhanced premium tax credits (APTCs).

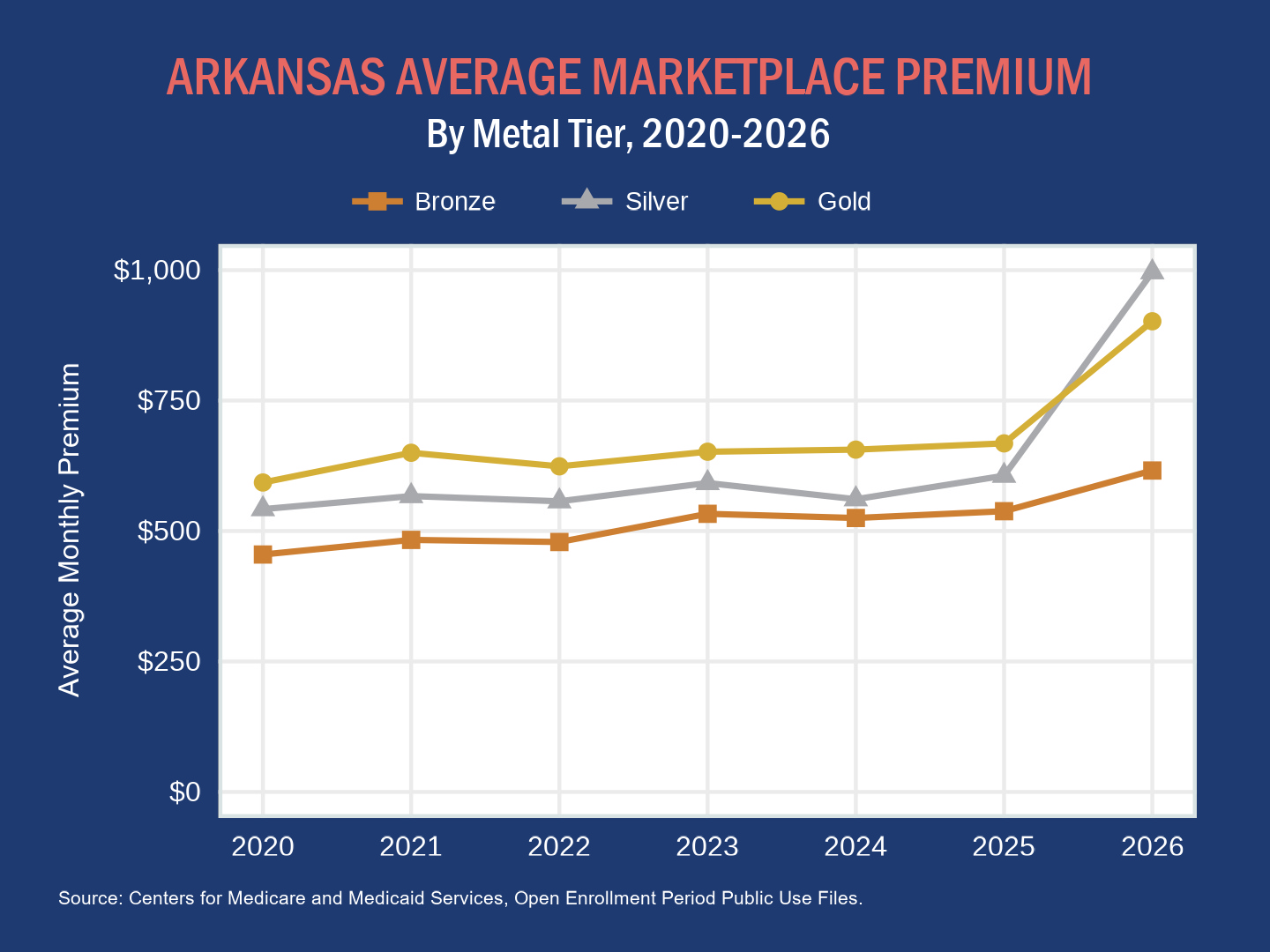

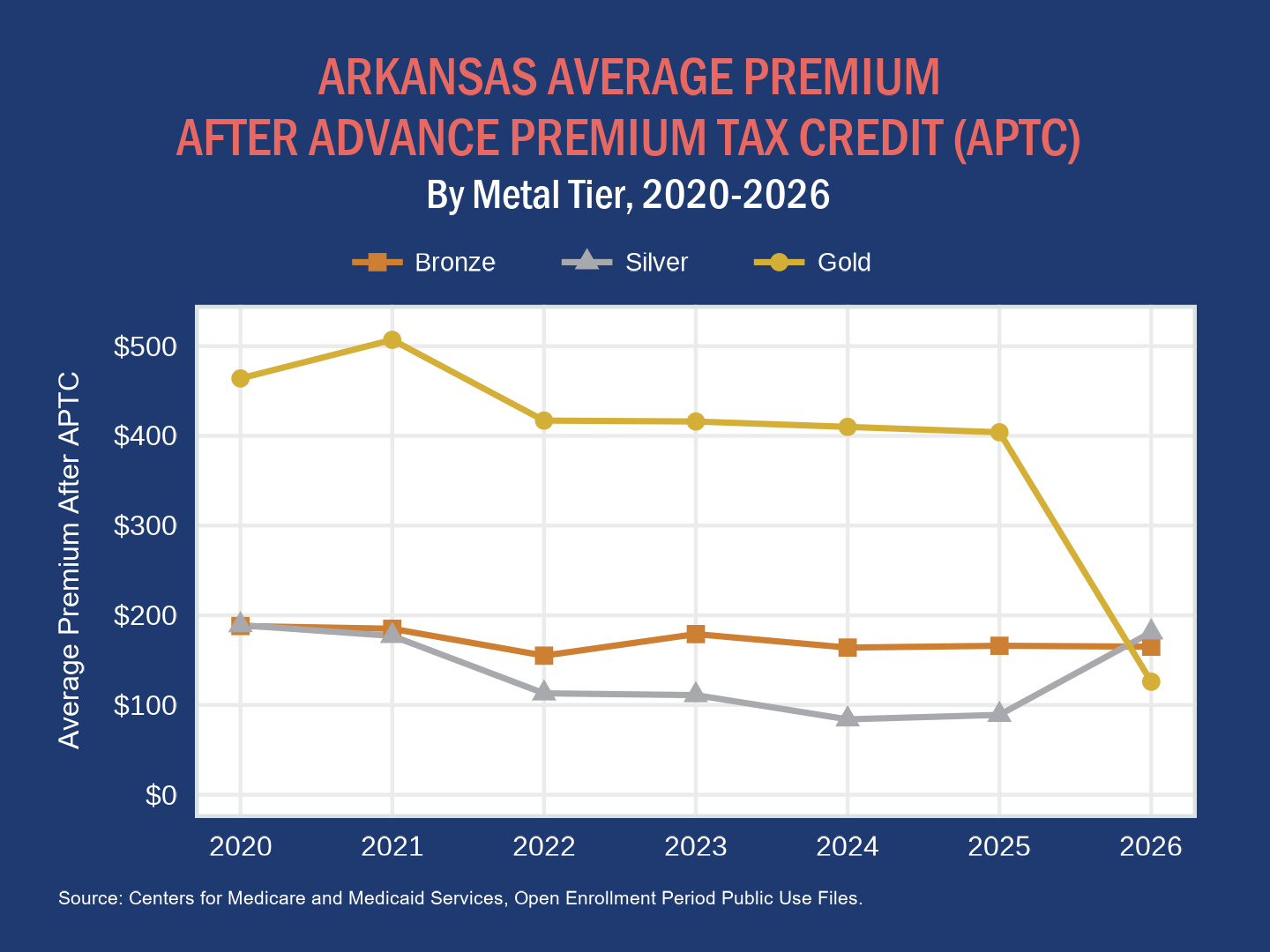

In February, we noted that Arkansas’s average benchmark premiums had increased for 2026 and that insurers had used a practice called “silver loading” to help reduce marketplace coverage costs for consumers with qualifying incomes.

Because financial assistance through premium subsidies is based on the benchmark silver premium, tax credits become larger when insurers increase silver plan premiums. Larger tax credits can then make gold plan premiums more competitive with, and even cheaper than, those of silver plans, depending on a consumer’s income.

The average silver premium in 2026 grew substantially more than that of bronze and gold plans. As a result, individuals with lower incomes — and thus large tax credits — moved overwhelmingly toward gold plans.

Arkansas insurers’ plan pricing strategy in 2026 fundamentally altered the balance between premiums and cost sharing for many marketplace enrollees. In our next post in this series, we will explore in greater detail how consumers responded to changing plan premiums.