Among the 10 states shown, Arkansas had the largest percentage increase in its statewide average pre-subsidy premium, but the smallest percentage increase in its average post-subsidy premium — which reflects the cost paid by consumers. That said, Arkansas’s average post-subsidy premium remained relatively high at $162 — the third-highest of the 10 states included in this comparison.

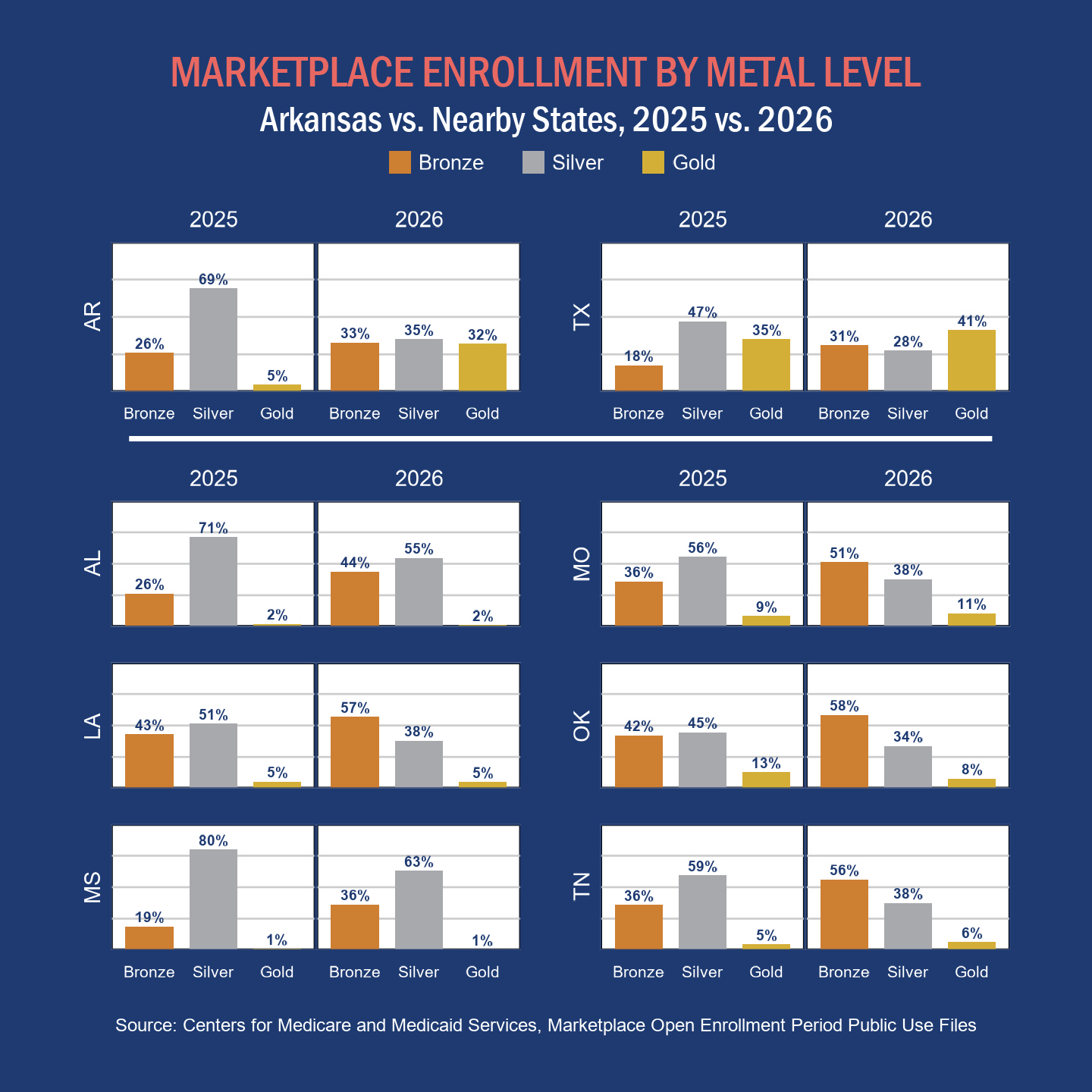

Shift in Metal Tier Enrollment: Arkansas vs. Nearby States

As discussed in our previous post on consumer shopping behavior in the 2026 open enrollment period, premiums vary widely between consumers within a state, primarily depending on income and metal level selection. Consumers in different states faced different marketplace circumstances, depending on what policy actions their states took to control rising health insurance costs.

In Arkansas, consumers shifted substantially from silver plans to gold plans. For silver plan enrollees with incomes that qualify them for little or no federal cost-sharing reductions, moving to a gold plan likely meant reduced cost-sharing exposure for little or no extra cost. For those who do qualify for cost-sharing reductions, the move to a gold plan likely meant higher cost-sharing exposure. However, for both groups, the shift to gold plans was a more favorable outcome than the swing toward low-premium, high-cost-sharing bronze plans seen in many peer states. The graphic below compares metal tier plan selections as a percentage of total marketplace enrollment in Arkansas and a selection of nearby states.

Arkansas and Texas experienced substantial growth in the proportion of enrollees who selected gold plans for 2026. Texas law has effectively required silver loading since 2023, so its enrollment in gold plans was already high in 2025. By implementing similar pricing dynamics, Arkansas saw a similar metal tier enrollment pattern in 2026. The other six states included did not implement silver loading to the same extent in 2026. In those states, movement was primarily from silver to bronze plans, which generally have higher cost sharing regardless of consumers’ income levels.

Effects of Differing Policy Approaches

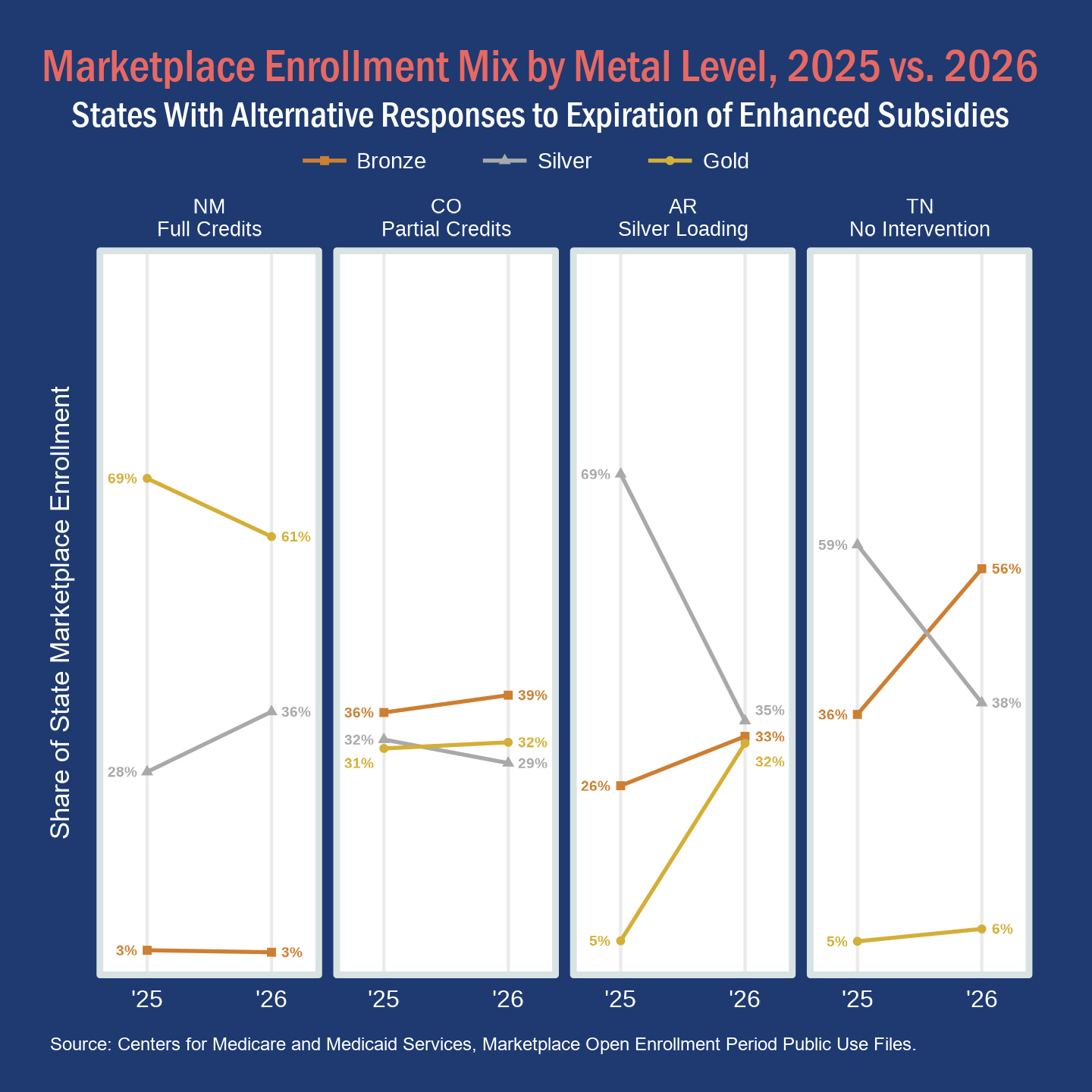

Some states took a more direct approach to reducing the cost of coverage for marketplace consumers as the enhanced premium tax credits expired at the end of 2025. New Mexico went farther than most states by using state funds to cover the expired federal subsidies in full for nearly all enrollees. Other states, such as Colorado, partially covered the credits for some enrollees.

New Mexico appropriated $22.3 million in general funds and an additional $17.3 million in emergency funds largely to continue the enhanced advance premium tax credits in full. The state experienced substantial growth in overall enrollment and saw a greater share of consumers selecting silver plans and a reduced share selecting gold plans. New Mexico already had disproportionately high enrollment in gold plans in 2025, partly because New Mexico, like Texas and Colorado, had implemented substantial silver loading prior to 2025. The shift from gold to silver may reflect in part an influx of new enrollees selecting New Mexico’s unique “turquoise plans” — a set of three marketplace plans (two silver and one gold) available since 2024 that use state subsidies to reduce cost sharing for eligible consumers. For lower-income consumers, these plans offer strong cost-sharing protections relative to their premiums and draw enrollment to the silver and gold metal tiers.

Colorado took a $100 million loan from a state trust fund and used the money to restructure an existing state subsidy program to offer a flat dollar subsidy to all enrollees with qualifying incomes and continue funding a reinsurance program. The reinsurance program, which pays insurers when the cost of claims exceeds a threshold amount, is intended to encourage insurers to reduce premiums. As a result of these measures, movement between the metal tiers in Colorado was relatively limited. Colorado’s 2025 metal tier enrollment breakdown is similar to Arkansas’s in 2026, as Colorado has effectively implemented a form of silver loading since 2019.

Tennessee had an enrollment breakdown comparable to Arkansas’s in 2025, but it did not silver load to the extent that Arkansas did in 2026, so like most of Arkansas’s other neighbors, Tennessee experienced a shift in enrollment toward bronze plans.

States that replaced some or most of the expired federal subsidies generally avoided a shift to enrollment in plans with greater cost exposure for consumers, but those approaches required substantial state funding. While Arkansas’s approach resulted in a move to gold plans that increased cost exposure for some consumers, it does appear to have prevented the broad shift toward bronze plans seen in many other states. For states where state-funded subsidies are not feasible, robust implementation of silver loading may offer an alternative policy option to reduce net premiums without additional state spending.

See also our previous posts in this series:

Arkansas Health Insurance Marketplace Data Show Changes in Enrollment, Plan Selection, Premiums

More Consumers on Arkansas Marketplace Shopped Around for Health Plans This Year, Data Show

This post was prepared with assistance from members of the University of Arkansas for Medical Sciences Fay W. Boozman College of Public Health, including Dr. Güneş Koru and students Jayli Holt, Brooklyn Torrence, and Annie Pro.